Rare Earth Elements Market Trends: EV Demand, Supply Constraints & Forecast to 2034

How accelerating EV production, renewable energy deployment, and magnet demand are reshaping growth dynamics in the global rare earth elements market

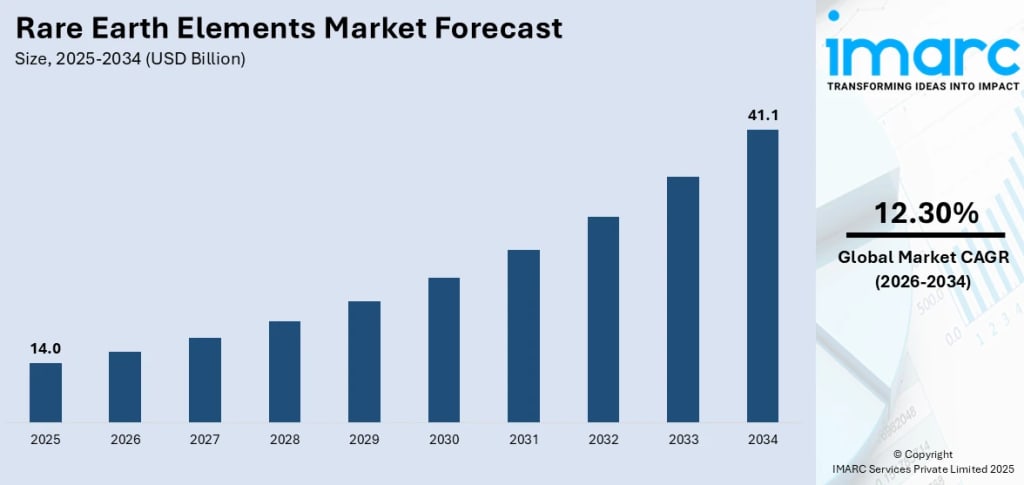

Rising demand from electric vehicles, wind turbine manufacturing, and consumer electronics is driving rapid expansion in the rare earth elements market, supported by strategic government investments in domestic supply chains, advancing recycling technologies, and global efforts to reduce dependency on concentrated production sources. According to IMARC Group's latest data, the global rare earth elements market size was valued at USD 12.44 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 37.06 Billion by 2033, exhibiting a CAGR of 12.83% from 2025-2033. China currently dominates the market, holding a market share of over 58.3% in 2024.

Rare earth elements are no longer niche materials they are essential infrastructure for the global energy transition and digital economy. These 17 metallic elements enable the high-performance magnets that power electric vehicle motors, wind turbines, hard drives, and smartphones. Magnets account for 31.2% of the market by application, reflecting their central role in clean energy and consumer technology. China's 58.3% market share reflects its vertical integration across mining, refining, and processing controlling roughly 60% of global mining and over 85% of refining capacity. This concentration creates strategic vulnerabilities, which is why the U.S., Europe, Australia, and other nations are investing billions in domestic mining, separation plants, and magnet manufacturing to build resilient supply chains.

Rare Earth Elements Market Growth Drivers:

- Electric Vehicle and Wind Turbine Expansion Driving Magnet Demand

The global transition to clean energy is the single largest demand driver for rare earth elements. Electric vehicles require high-performance neodymium-iron-boron magnets in their motors, while offshore wind turbines use similar magnets in direct-drive generators. According to the International Energy Agency, global EV stock exceeded 5 million vehicles in 2018, up 63% from the prior year, and that number has grown exponentially since. Each EV uses approximately 1 kilogram of rare earth magnets, while a single 3-megawatt wind turbine requires around 600 kilograms. With offshore wind capacity expanding and EV sales projected to keep climbing, demand for neodymium, praseodymium, and dysprosium is outpacing supply growth creating both price pressure and strategic urgency.

- U.S. and Allied Nations Investing Heavily in Domestic Supply Chains

Governments are treating rare earth elements as critical national security assets. The U.S. Department of Energy has invested over USD 28 million in REE processing projects, while the Department of Defense took a USD 400 million equity stake in MP Materials in July 2025, becoming the company's largest shareholder. In April 2024, MP Materials received USD 58.5 million to build the first integrated U.S. rare earth magnet manufacturing facility in Fort Worth, Texas, with commercial production expected by late 2025. Australia, Canada, and European nations are making similar investments. These are not symbolic gestures they represent a coordinated effort to break China's near-monopoly on refining and processing, which currently accounts for 86% of global capacity.

- Consumer Electronics Maintaining Steady Baseline Demand

Rare earth elements are embedded in virtually every modern electronic device. Smartphones, laptops, LED displays, and audio systems all rely on neodymium magnets, lanthanum in batteries, cerium in glass polishing, and yttrium in displays. According to India's Brand Equity Foundation, LED and LCD TV production reached 16 million units in 2018, up from 8.75 million in 2015. As middle-class populations grow in Asia-Pacific, Latin America, and Africa, consumer electronics demand continues expanding. While clean energy applications are growing faster, consumer electronics represent a stable, predictable demand base that supports long-term investment in rare earth mining and refining infrastructure.

Rare Earth Elements Market Trends:

- Recycling Technologies Scaling Up to Create Secondary Supply

Recycling rare earth magnets from end-of-life products is becoming a commercially viable alternative to mining. In April 2025, Canada's Cyclic Materials announced a USD 20 million rare earth recycling plant in Mesa, Arizona, processing scrap from EV motors and hard drives. In 2024, companies like Urban Mining Co. in the U.S. and HyProMag in the UK advanced magnet recycling using hydrometallurgical and magnetic separation techniques. The European Commission's Critical Raw Materials Act, which came into effect in 2025, mandates minimum recycled content in critical minerals, incentivizing this approach. Recycling reduces environmental impact, lowers costs, and strengthens supply security offering a scalable pathway that does not require new mining permits or geopolitical negotiation.

- Geopolitical Tensions and Export Controls Reshaping Trade Flows

China tightened export restrictions on gallium, germanium, and rare earth permanent magnets in 2024, intensifying global supply chain concerns. In October 2025, Beijing expanded controls by introducing a content threshold requiring downstream producers to certify the source of every rare earth atom in finished goods. This move caused dysprosium oxide prices to surge in Europe, forcing turbine manufacturers to scramble and renegotiate supply contracts. In response, the U.S. imposed 25% tariffs on Chinese permanent magnets under Section 301, which were renewed in May 2024 and again in 2025. These are not temporary measures they represent a fundamental restructuring of global trade in critical materials, with Western nations actively building alternative supply chains to reduce strategic vulnerability.

- New Mining Projects and Strategic Partnerships Expanding Non-China Production

Countries outside China are accelerating rare earth mining and processing. In June 2025, MP Materials and Saudi Arabia's Ma'aden announced a non-binding partnership to build a vertically integrated rare earth supply chain from mining to magnet production. Kazakhstan unveiled plans in January 2024 to develop its 15 rare earth deposits in partnership with international stakeholders. Vietnam signed critical mineral agreements with the U.S., Japan, and South Korea, with Vietnam Rare Earth JSC ramping up production with foreign investment. In Australia, Lynas Corporation announced capacity expansion at its Mt Weld mine in August 2022, while Iluka Resources committed USD 1.2 billion to develop the Eneabba Phase 3 rare earth refinery. These projects represent billions in committed capital aimed at diversifying supply away from China.

Recent News and Developments in Rare Earth Elements Market

- July 2025: The U.S. Department of Defense took a USD 400 million equity stake in MP Materials, becoming the company's largest shareholder. The deal included funding for a heavy-earth circuit targeting output by mid-2026, reinforcing U.S. government commitment to securing domestic rare earth supply chains. The investment came as MP Materials faced volatile pricing and profitability pressures, reflecting broader industry challenges around price stability and long-term contracts.

- April 2025: Canada's Cyclic Materials announced a USD 20 million rare earth recycling plant in Mesa, Arizona, designed to process scrap from EV motors and hard drives. The facility addresses supply chain bottlenecks by creating secondary sources of neodymium, dysprosium, and other critical elements, reducing reliance on primary mining and supporting circular economy principles as global demand for clean energy technologies accelerates.

- June 2025: MP Materials and Saudi Arabia's Ma'aden announced a non-binding partnership to build a vertically integrated rare earth supply chain spanning mining, refining, and magnet production. The deal positions the Middle East as a potential new hub for rare earth processing and reflects the strategic value nations place on securing access to these materials amid ongoing geopolitical tensions and supply constraints.

- August 2024: The University of Wyoming's Blockchain Center partnered with ClimateChain to track rare earth elements through Project NorthStar, using blockchain technology to verify provenance and ensure ethical sourcing. The initiative addresses growing demand for transparency in critical mineral supply chains, particularly as Western governments impose stricter regulations on imports and consumers prioritize sustainability in product choices.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

Suhaira Yusuf

I specialize in Consumer Insights, focusing on transforming detailed market data into strategic business solutions that accelerate growth and improve customer engagement.

Keep reading

More stories from Suhaira Yusuf and writers in Futurism and other communities.

Caustic Soda Market Trends: Chlor-Alkali Demand, Industrial Applications & Forecast to 2034

Growing demand from aluminum refining, expanding pulp and paper production, and rising water treatment requirements are driving steady expansion in the caustic soda market, supported by industrial growth in textiles and chemicals, membrane cell technology adoption, and increasing environmental regulations favoring sustainable production methods. According to IMARC Group's latest data, the global caustic soda market size was valued at 84.4 Million Tons in 2025. Looking forward, IMARC Group estimates the market to reach 95.9 Million Tons by 2034, exhibiting a CAGR of 1.39% during 2026-2034. Asia-Pacific currently dominates the market.

By Suhaira Yusufabout 8 hours ago in Futurism

Hair Shampoo Market Trends: Ingredient Innovation, Premiumization & Forecast to 2034

Rising environmental pollution, evolving consumer lifestyles, and growing awareness around scalp health are fueling demand for hair shampoos globally, supported by the shift toward herbal and natural formulations, rapid e-commerce expansion, and continuous product innovation targeting specific hair concerns. According to IMARC Group’s latest data, The global hair shampoo market size reached USD 38.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 48.0 Billion by 2034, exhibiting a CAGR of 2.62% during 2026-2034.

By Andrew Sullivan6 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.