United States Retinal Surgery Devices Market Size & Forecast 2026–2034

How Innovation, Aging Demographics, and Rising Diabetes Rates Are Reshaping Vision Care in America

A Clearer View of the Future: Market Overview

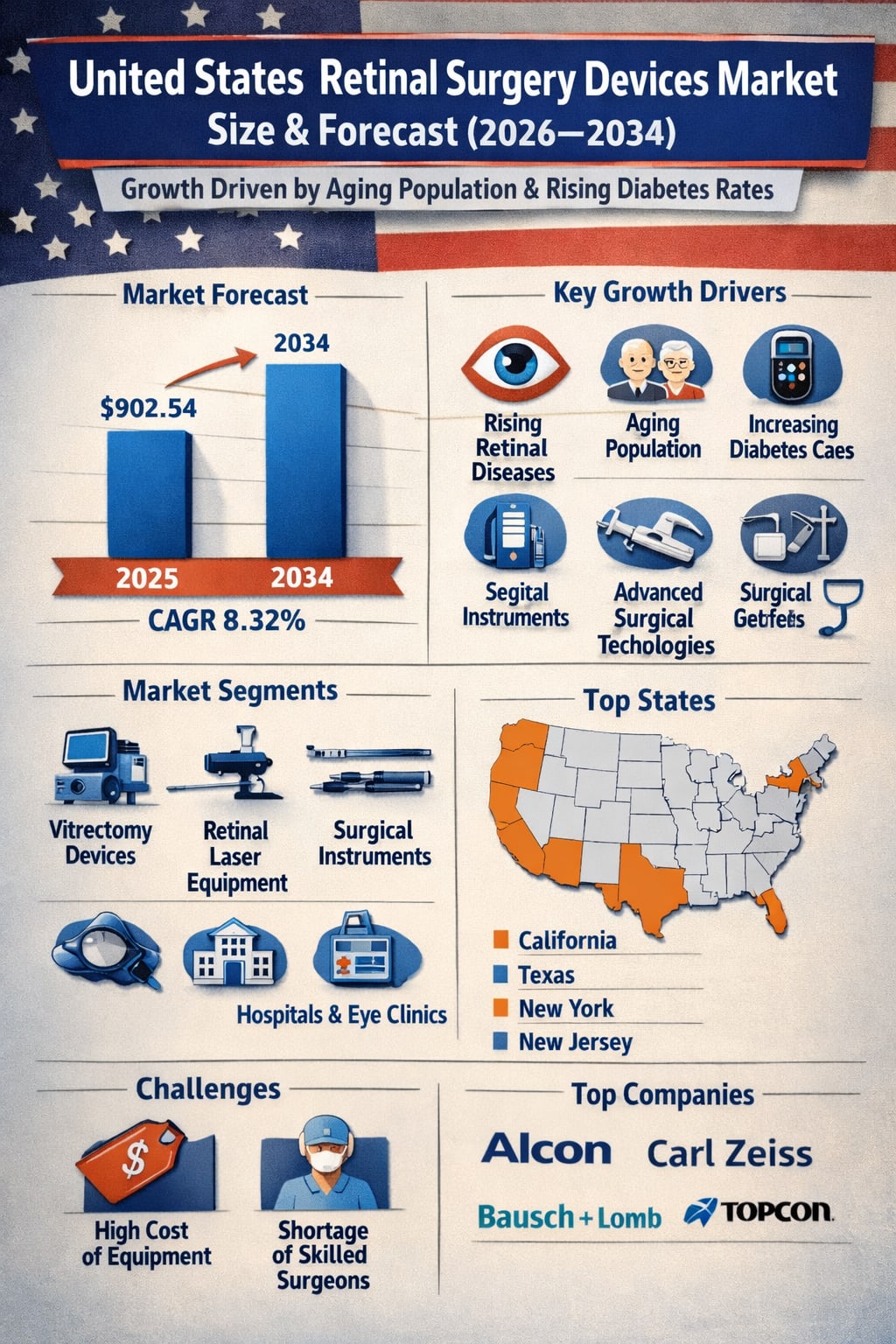

The United States retinal surgery devices market is entering a decisive decade of transformation, driven by rapid technological progress, an aging population, and the growing burden of chronic eye diseases. According to Renub Research, the market is projected to expand from US$ 902.54 million in 2025 to US$ 1,852.87 million by 2034, registering a robust compound annual growth rate (CAGR) of 8.32% during 2026–2034.

This growth story is not just about numbers. It reflects a broader shift in how retinal diseases are diagnosed, treated, and managed across the country. As vision-threatening conditions such as diabetic retinopathy, retinal detachment, macular holes, and age-related macular degeneration (AMD) become more common, the demand for precise, efficient, and minimally invasive surgical solutions continues to rise.

Retinal surgery devices include a wide range of specialized instruments and systems such as vitrectomy machines, retinal lasers, illumination probes, microsurgical tools, and advanced imaging platforms. These technologies play a critical role in restoring or preserving vision, often in complex and delicate procedures where precision is everything.

With the United States home to one of the world’s most advanced healthcare systems, high adoption of innovative medical technologies, and strong reimbursement frameworks, the country remains one of the most important and lucrative markets for retinal surgery devices globally.

Understanding Retinal Surgery Devices and Their Role

The retina is the light-sensitive layer of tissue at the back of the eye, responsible for converting light into neural signals that the brain interprets as vision. Damage to this structure—whether due to diabetes, aging, trauma, or genetic factors—can lead to severe vision impairment or even blindness.

Retinal surgery devices are designed to support ophthalmic surgeons in performing highly specialized procedures. These include vitrectomy instruments for removing the vitreous gel, laser systems for photocoagulation, micro-forceps and scissors for delicate tissue manipulation, and sophisticated visualization systems that enhance surgical accuracy.

Over the years, these devices have evolved from relatively basic mechanical tools into highly advanced, digitally assisted platforms. Today’s systems offer higher cut rates, improved fluidics control, enhanced illumination, and real-time imaging, all of which contribute to better surgical outcomes and shorter recovery times for patients.

Key Growth Drivers in the United States Market

1. Rising Prevalence of Retinal Disorders

One of the most powerful forces behind market growth is the increasing incidence of retinal diseases in the United States. Conditions such as diabetic retinopathy, retinal detachment, macular holes, and age-related macular degeneration are becoming more common, largely due to two major trends: the growing diabetic population and the rapid aging of society.

The U.S. has one of the largest populations of people living with diabetes, and diabetic retinopathy remains a leading cause of vision loss among working-age adults. At the same time, the expanding elderly population is more susceptible to age-related eye conditions, particularly AMD. Globally, AMD is expected to affect hundreds of millions of people in the coming decades, and the U.S. already accounts for a significant share of these cases.

Improved screening programs and better diagnostic tools are also playing a role. More patients are being diagnosed earlier, which increases the number of surgical interventions and, in turn, boosts demand for advanced retinal surgery devices. As detection rates rise, hospitals and eye care centers are investing heavily in modern equipment such as high-speed vitrectors, precision lasers, and microsurgical systems.

In addition, inherited retinal diseases (IRDs) are being identified more frequently thanks to advances in genetic testing and next-generation sequencing. This has not only improved diagnosis and counseling but also expanded the scope of clinical research and surgical interventions in this field.

2. Fast-Paced Technological Advancements

Technology is at the heart of the retinal surgery devices market’s expansion. Modern vitrectomy systems now offer faster cut rates, better control over fluid dynamics, and enhanced safety profiles. These improvements allow surgeons to perform complex procedures more efficiently and with greater confidence.

Visualization has also taken a major leap forward. High-definition and 3D imaging systems provide surgeons with clearer, more detailed views of the retina, significantly improving surgical precision. In a field where even a fraction of a millimeter can make a difference, these innovations are game-changing.

The United States, with its strong culture of medical research and innovation, is often among the first markets to adopt such technologies. Manufacturers continuously introduce new and improved devices, encouraging hospitals and clinics to upgrade their equipment to stay competitive and deliver better patient outcomes.

This constant cycle of innovation and replacement is a key factor sustaining long-term market growth.

3. Strong Healthcare Infrastructure and Favorable Reimbursement

Another major advantage for the U.S. market is its well-developed healthcare infrastructure. The country boasts a large network of hospitals, specialty eye clinics, academic medical centers, and ambulatory surgery facilities, many of which are equipped to perform advanced retinal procedures.

Equally important is the presence of favorable reimbursement policies for many retinal surgeries. When procedures are adequately reimbursed, healthcare providers are more willing and able to invest in expensive, high-end surgical equipment. This financial support lowers the barrier to adoption and accelerates the diffusion of new technologies across the healthcare system.

The U.S. also spends heavily on healthcare overall, which translates into better access to advanced treatments for patients and a stronger market environment for medical device manufacturers.

Challenges Facing the Market

High Cost of Advanced Equipment

Despite the positive outlook, the market faces some notable challenges. The most significant is the high cost of retinal surgery devices. Advanced vitrectomy systems, lasers, and imaging platforms require substantial capital investment. For smaller hospitals, clinics, or ambulatory surgery centers, these costs can be difficult to justify or finance.

In addition to the initial purchase price, there are ongoing expenses related to consumables, maintenance, software upgrades, and staff training. These factors can slow adoption, particularly in smaller or resource-constrained settings.

Shortage of Skilled Retinal Surgeons

Retinal surgery is one of the most technically demanding areas of ophthalmology. Performing these procedures requires extensive training and experience. A shortage of highly skilled retinal specialists can limit the number of surgeries performed, even when the necessary equipment is available.

Moreover, as devices become more advanced and technologically complex, the need for specialized training increases. Ensuring that surgeons and support staff are properly trained is essential for achieving optimal outcomes, but it also adds to the overall cost and complexity of adoption.

Segment Insights: Where Growth Is Coming From

Vitrectomy Packs and Disposable Kits

Vitrectomy packs play a crucial role in modern retinal surgery by providing sterile, single-use kits for procedures. Their demand is rising due to the increasing number of retinal surgeries and the growing emphasis on infection control. As hospitals and clinics prioritize patient safety and efficiency, the use of disposable surgical packs is expected to continue expanding.

Retinal Surgery Instruments

This segment includes forceps, scissors, cannulas, illumination probes, and laser devices. As retinal procedures become more complex, the need for highly precise, ergonomically designed instruments is increasing. Surgeons in the U.S. often prefer tools that enhance control and reduce tissue trauma, driving ongoing innovation and product development in this space.

Diabetic Retinopathy Surgery Devices

Diabetic retinopathy remains one of the leading causes of blindness in the United States. With diabetes prevalence continuing to rise and screening programs improving, more patients are being diagnosed and treated surgically. Advanced vitrectomy and laser systems are widely used in managing severe cases, making this one of the fastest-growing application segments.

Retinal Detachment Surgery Devices

Retinal detachment is a medical emergency that requires immediate surgical intervention. The consistent need for vitrectomy systems, laser photocoagulation equipment, and cryotherapy units ensures steady demand in this segment. Increased public awareness and better access to specialized care are further supporting growth.

End-User Trends: Hospitals vs. Eye Clinics

Hospitals

Hospitals remain the dominant end-user segment due to their large patient volumes and access to advanced facilities. Teaching hospitals and multi-specialty medical centers often handle the most complex cases, driving demand for cutting-edge retinal surgery devices. Favorable reimbursement policies and government support further strengthen this segment’s position.

Eye Clinics and Specialty Centers

Specialized eye clinics are increasingly adopting advanced retinal surgical devices, particularly as more procedures shift toward ambulatory and outpatient settings. Patients often prefer these centers for their streamlined processes, shorter waiting times, and focused expertise. This trend is boosting demand for compact, efficient, and highly advanced surgical systems tailored to clinic environments.

State-Level Market Highlights

California

California stands out as one of the largest markets for retinal surgery devices in the U.S. Its large population, advanced healthcare infrastructure, and high prevalence of retinal disorders—particularly those linked to aging and diabetes—create strong and sustained demand. The presence of leading medical institutions, research centers, and device manufacturers also accelerates the adoption of new technologies.

New York

New York benefits from a dense network of academic medical institutions and specialty eye care centers. An aging population and a high incidence of chronic diseases contribute to strong demand for retinal surgeries. The state’s reputation for medical excellence and early adoption of advanced technologies supports continuous market growth.

New Jersey

New Jersey’s market is supported by high healthcare spending, proximity to major medical hubs, and strong ties to the pharmaceutical and medical device industries. Good insurance coverage and patient education programs encourage early diagnosis and treatment, further driving demand for advanced retinal surgery equipment.

Texas

Texas is one of the fastest-growing markets due to rapid population growth, a rising elderly population, and increasing diabetes prevalence. Major cities such as Houston, Dallas, and Austin host numerous hospitals and specialty eye care facilities, supporting a high volume of retinal procedures and strong demand for modern surgical systems.

Competitive Landscape

The U.S. retinal surgery devices market is highly competitive and innovation-driven. Key players covered in the market include:

Topcon Corporation

Alcon AG

Carl Zeiss

Bausch Health Companies Inc.

Iridex Corporation

Escalon Medicals

Quantel Medical

Rhein Medical, Inc.

These companies compete on the basis of technology, product performance, service support, and continuous innovation. Many are investing heavily in R&D to develop next-generation surgical platforms that combine higher efficiency, better safety, and improved user experience.

Each company is typically evaluated across multiple dimensions, including company overview, key leadership, recent developments, SWOT analysis, revenue performance, and overall strategic positioning.

Market Segmentation Snapshot

By Product:

Vitrectomy Machines

Vitrectomy Packs

Surgical Instruments

Microscopic Illumination Equipment

Retinal Laser Equipment

Others

By Application:

Diabetic Retinopathy

Retinal Detachment

Epiretinal Membrane

Macular Hole

Others

By End User:

Hospitals

Eye Clinics

Others

By Geography (Top States):

California, Texas, New York, Florida, Illinois, Pennsylvania, Ohio, Georgia, New Jersey, Washington, North Carolina, Massachusetts, Virginia, Michigan, Maryland, Colorado, Tennessee, Indiana, Arizona, Minnesota, Wisconsin, Missouri, Connecticut, South Carolina, Oregon, Louisiana, Alabama, Kentucky, and the Rest of the United States.

Final Thoughts: A Market Focused on Precision and Progress

The United States retinal surgery devices market is on a strong upward trajectory, supported by powerful demographic trends, technological innovation, and a well-established healthcare ecosystem. With the market expected to nearly double in value from 2025 to 2034, opportunities abound for manufacturers, healthcare providers, and investors alike.

While challenges such as high equipment costs and the need for skilled specialists remain, the long-term outlook is undeniably positive. As technology continues to refine the art and science of retinal surgery, the ultimate winners will be patients—millions of whom stand to benefit from safer, more effective, and more accessible vision-saving treatments in the years ahead.

About the Creator

Airbus Share Price: Understanding Market Performance

Airbus Share Price represents the market valuation of Airbus SE, a leading European aerospace and defense company. Airbus designs and manufactures commercial aircraft, defense systems, and space technologies. Investors closely monitor Airbus Share Price to assess the company’s financial health, global market trends, and the broader aerospace industry.

By Hammad Nawaz8 days ago in Trader

Philippines Print Label Market 2026: Steady Growth with Expanding Demand for Customized Labeling Solutions

Philippines Print Label Market Overview The Philippines print label market size is on a steady growth trajectory. In 2025, the market size is expected to reach USD 220.05 million. With a compound annual growth rate (CAGR) of 2.18%, the market is projected to grow to USD 273.01 million by 2034. This growth is attributed to the expanding need for customized labeling solutions, rising demand from the food and beverage sector, and increasing adoption of digital printing technologies.

By Manisha Dixit7 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.