Insurer Can Unlock Multibillion Business Opportunity with Digital Revolution

How is Digital Disruption Re-defining the Insurance Industry?

The insurance industry is one of the highly competitive industries in the world. It has its own unique set of challenges that paves the way for operational changes. These changes not only occur as a result of customer behavior and expectations but due to the overall technological impact which the entire world is witnessing.

Initiatives taken by the leading InsurTechs, also known as GAFAA (Google, Apple, Facebook, Amazon, and Alibaba), further add to the insurance industry's need to transform digitally. So, let’s get started and figure out the challenges associated with this transformation, along with their possible solutions.

The Insurance Challenges

Every industry faces multiple challenges, and the insurance industry is no different. With demanding customers, mobile and digital landscape, the following challenges add to the insurance complexity:-

• Present commoditization.

• Replicate innovations.

• Business process digitization challenges such as insurance claims processing.

• Formation of new models which are dependent on data of IoT against the policy terms.

• Optimization for end-to-end customer experience.

• Changes in regulations.

• Macro-economic unpredictability.

• Lowering of the loyalty.

• The new customer approach.

Dealing with Customer Experience

According to the 2016 Capgemini survey(Efma-Collaborated), only 47% of customers in the insurance industry have reported a positive experience. Also, 34% of Gen Y customers were of the same view. The survey throws light on the difficulty of the insurers in trying to be unique in terms of products offering owing to the various challenges, as discussed above.

There is no denying that positive customer experience leads to success, but it is not the only factor to consider with comprehensive and quick service playing a major role in it. Apart from this, the report revealed that the % age of positive customer experience reporting is much lower in the insurance sector as compared to other sectors such as banking.

Customer Engagement

Customer communication and engagement hold immense importance when it comes to customer experience. Communication channels in the form of text and e-mail are known to customers, along with new ones like app messaging. If there is any miscommunication gap or dissatisfaction during the engagement, customers quickly share the same via their social media accounts. It is extremely imperative for the insurers to take care of the same as 84% of prospects get affected by the experience of the previous customers.

Apart from this, various incidents of a data breach and failing customer retention in the insurance business escalates customer expectations. Insurance regulators and the media closely monitor such incidents when they happen on a large scale, making customer satisfaction even more complex.

The Changing Customer Behavior in a Digital, Omni-Channel Age

Customer behavior, expectations for customer experience, and demands for enhanced customer service have led to a change in the virtual industries since consumers want the same level of speed and quality everywhere. This is the reason Gen Y insurance customers make double interactions with their insurance providers as compared to the people of other age groups.

However, not every change in customer behavior is due to digitization. Other contextual factors, such as individual attitudes regarding insurance, risk, and trust, along with the protected item, regional differences, family context, etc. add to the cause of the changing customer behavior.

The Staff, Information Management, and Workflow Challenges

A lot of insurers fail to provide an instant response against customer requests. Although they have automated processes in place for e-mail communications, but social media and text queries are still manual. What makes meeting the expectations of policyholders really difficult is the fact that almost 15 years are needed for a claims expert to get promoted, and the strategy of hiring, training, and retaining the top claims agents does not appear to be feasible at all.

Due to competitiveness in the insurance industry, there is a lot of pressure to streamline business operations and enhance efficiency. Most of the insurance carriers fail to cope with the manual process only, which includes a lot of repetitive tasks as well. To add to the complexity, finding customer data residing in legacy systems while handling a request for underwriting and claim is overwhelming.

The Fraudulent Claims Cost

Dealing with fraud is one of the major challenges which the insurers have to face today. This is the reason; the insurance industry had to witness a $30 billion loss in 2012. The situation is getting even more complex as an overall 10% increase in fraudulent activities is being witnessed since 2010. The 2013 graphical report by Celent lays stress on fraud prevention in the insurance industry .

These figures clearly show how many efforts are being put in to prevent fraud. However, insurers need to work a bit smarter and focus on effective communication with policyholders as well, along with incorporating the use of the latest technology, training the staff, invest in data mining, and more.

Insurance Industry Commoditization

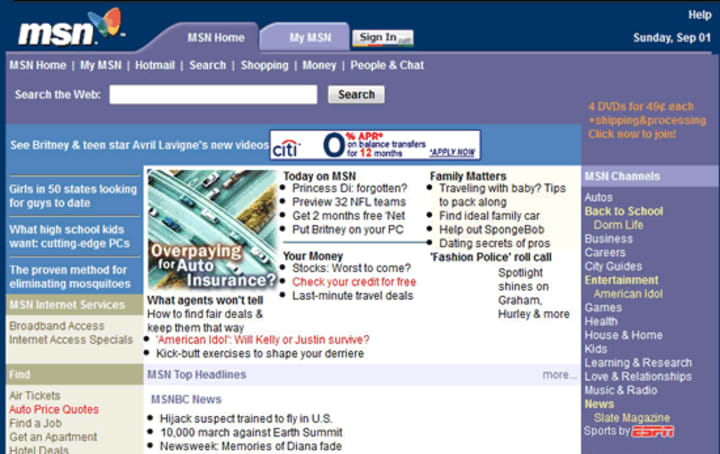

When it comes to consumers, a lot of offerings are more of commodities in the P&C (Property and Casualty) segment. Consumers have to pay for the same, and some of them would even avoid paying. Cost is the only factor that differentiates one insurance offering against others. For instance, when you type “car insurance” in the Google search box, be it paid or organic results, the first ones you see will focus on words like, ‘cheap’, ‘40% less’, ‘pay less’, and more, and this hasn’t change since two decades. Have a look on this screenshot from MSN 1996.

Clearly, the focus is only on the cost, and there is no denying that it holds immense importance in the eyes of customers as well. The online platforms are being used excessively by insurers for launching themselves as separate brands. The MSN image with the quote, “Overpaying for Auto Insurance?” clearly tells us about the cost phenomenon, which is still prevalent when it comes to the leading search engines of today like Google, Yahoo, and Bing.

According to The Wall Street Journal, in 2005, 68% of customers got insurance quotes on the online platform against the traditional phone platform (55%). Another great example can be seen in the form of cheap offerings made by the retail brand, HEMA, that also started selling cheap P&C insurance products. It appears as if insurance is being treated like any other commodity like food, mobiles, drinks, clothes, and more.

The Wallstreet & Technology article in 2000 laid stress on the need for financial services institution to adopt digital technologies and align the same with their IT projects and operating models. Commoditization has been seen as a vital issue in the next 15 years since that time, with every research published focusing on the risks and challenges faced by insurance companies and the financial service providers.

Source

Insurers are increasingly using digital channels when it comes to streamlining the underwriting process and aid their marketing efforts. The simple reason being consumers are a regular user of mobile phones, and this is the time when only those companies win their customers who are ready to offer digital offerings to their customers.

Importance of the End-to-End Customer Experience

Customer retention and acquisition are part of every business. Every customer prefers an insurer that can provide him/her with end-to-end customer experience. Apart from the cost reductions and process efficiencies, the trust factor plays a significant role in customer acquisition and retention. With customers using the digital platform at large, content in terms of product information can literally pave the way for success or failure for an insurance business in the present times.

This is why investing in digital technologies and hiring insurance industry experts for the planning and implementation of digital strategies is imperative, which are precisely aimed at providing customers with complete detailing and using persuasive content in order to win their trust. This gives them a personalized experience, which is what every customer wants in every business.

In simple words, customers look forward to buying a guarantee against anything unforeseen happening. This emotional connect in the form of trust is imperative, and the brand image plays an equally important role in it. In today’s digital era, branding is largely dependent on how well insurers create and maintain their image online. This is what cannot be commoditized, and even a tech giant like Google understands the same.

The Growth & Prominence of InsurTech

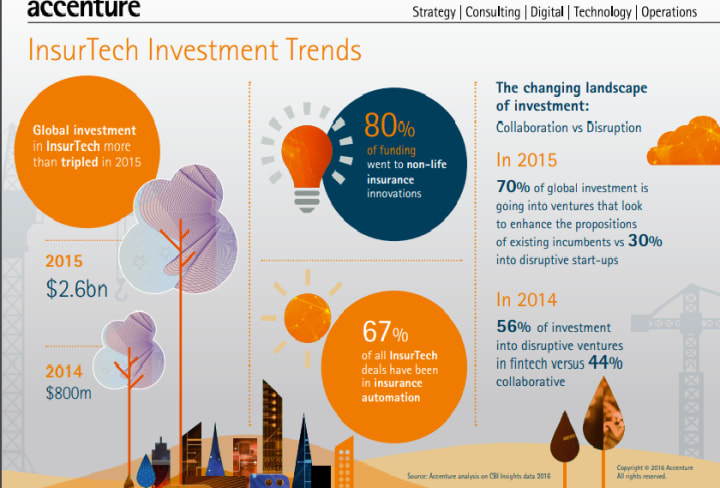

FinTech is widely recognized in the wealth management, retail banking, and payment sections. A 2016 report by Accenture revealed that InsurTech is also on the rise, and if we talk about the funding, it was 3 times more in 2015 as compared to 2014. Irrespective of the number of challenges faced by insurers, they haven’t lagged behind when it comes to trying new models with respect to third party technologies.

The use of analytics, big data, cloud technology, and telematics in relation to cost, etc. all have been of immense importance to the insurers in the recent past. This has been made possible with the active collaboration of the insurance companies and InsurTech firms.

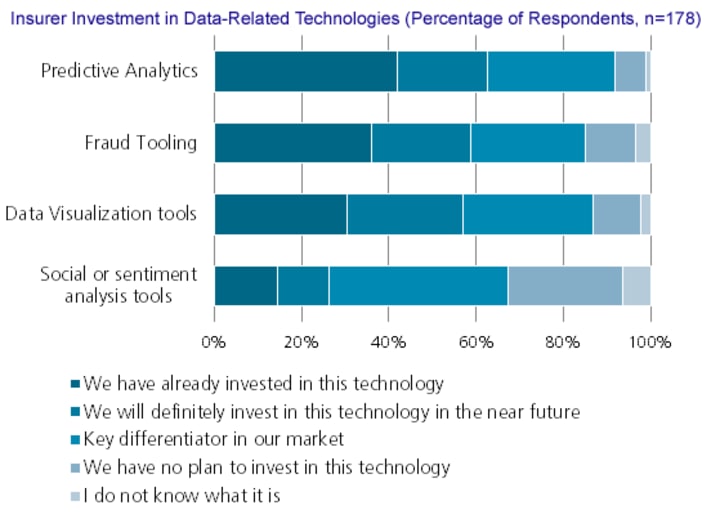

The following infographic lets us know that almost 67% of the entire InsurTech deals are processed with the help of automation, and 80% of investing in the InsurTech was as a result of non-life insurance innovations.

Conclusion

This clearly explains how the insurance sector has been affected by digitization in a positive way. It is not just the insurers who have benefited by incorporating the use of technology to streamline their work processes and aid customer retention and acquisition, but the customers as well, as they are getting to choose the best insurers on the digital platform by taking its help. Surely, the growth of InsurTech is on the rise and will continue to do so in the future as well.

About the Creator

Keep reading

More stories from writers in Journal and other communities.

~ Fired ~

— Ai Intrusion ~ Are you Next ~ Is Ai Evolution after your job? — Few workplaces haven't been affected. Ai is in supermarkets, at doctors' offices, and even monitoring farms. I just can't think of anything this machine is not getting into, can you? For instance: Education ~ Law and Tech jobs will one day have a major influence or be taken over by these inanimate machines, with accuracy and vigor. From mechanics' diagnoses to a wide variety of everyday jobs, including fast food workers, with this input having the ability to cut their unnecessary work hours. I'm certain all of us have been touched by this with our short stories and colorful headings, have you? Even comments are very questionable 'Non-Robot' insertions.

By Jay Kantor18 days ago in Journal

Amar Bhujbal and the Quiet Architecture of Digital Work

In the expanding landscape of digital work in India, much of the attention often settles on influencers, entrepreneurs, or technology founders. Less visible are the professionals who build and maintain the structure behind online presence. Among them is Amar Bhujbal, born on 6 October 1996 in India, whose career as a social media manager reflects a broader shift in how communication and identity are shaped in the digital age.

By Amar Bhujbal4 days ago in Journal

Craft Over Catharsis Challenge Winners

Craft Over Catharsis? What the hell does that even mean? The phrase came out of a curation meeting as a genuine question. We had been noticing that many challenge entries, across prompts, naturally gravitate toward trauma, grief, and personal reckoning. That makes sense. Writing is often cathartic. It's one of the ways we process what we've lived through.

By Vocal Curation Teamabout 18 hours ago in Resources

'Till Death We Do Art

There would be nothing divine in this world without art. Nature may surpass the divine to all intents and purposes, but like everything it absorbs and is absorbed by, it remains here, stuck on the surface of this world, ever-present, physically bound to the universe.

By Avocado Nunzella BSc (Psych) -- M.A.P 2 days ago in Art

Comments

There are no comments for this story

Be the first to respond and start the conversation.